How Much Do Braces Cost Per Month? (2026 Payment Plan Guide)

Quick Answer

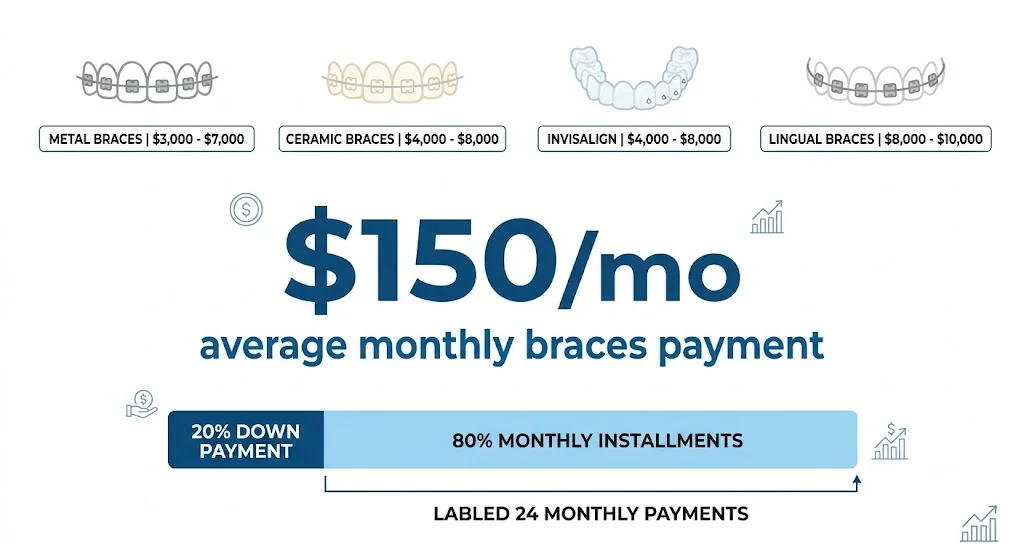

Most patients pay $100 to $250 per month for braces, based on a total treatment cost of $3,000 to $6,000 spread over 18 to 24 months. Orthodontic offices typically collect a down payment of 15 to 25% upfront and finance the remainder in-house at 0% interest. Monthly payments are lower when insurance covers part of the total, when you extend the payment period, or when you pay the full balance upfront for a cash-pay discount.

Part of our Braces Cost & Insurance Master Guide.

1. Monthly Cost by Braces Type

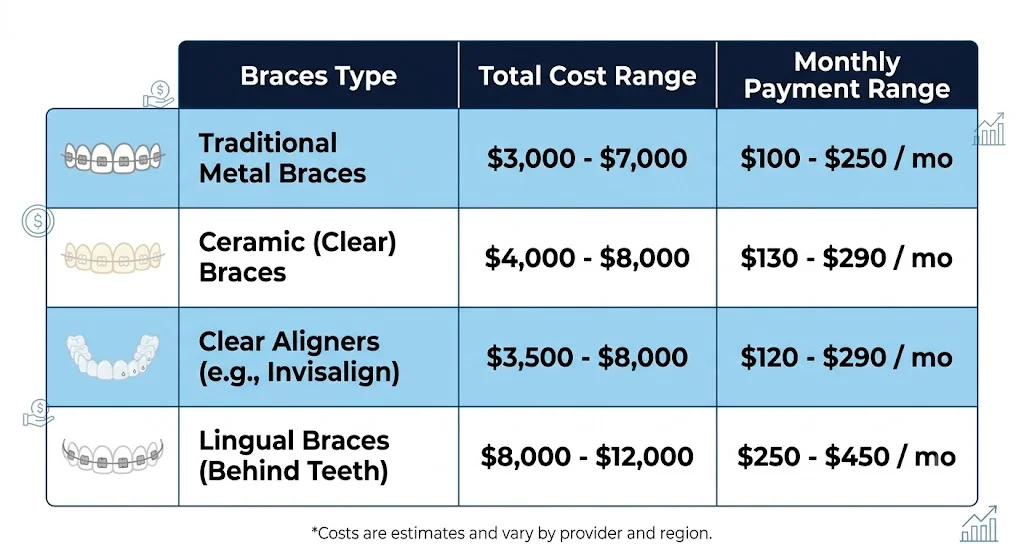

The monthly payment you make depends entirely on the total treatment fee and the length of your payment plan. Here is how the numbers break down by braces type, assuming a 24-month payment plan and no insurance:

| Braces Type | Typical Total Cost | Monthly Payment (24 mo.) |

|---|---|---|

| Metal braces | $3,000 – $5,500 | $125 – $229 |

| Ceramic braces | $4,000 – $7,000 | $167 – $292 |

| Clear aligners (Invisalign) | $3,000 – $8,000 | $125 – $333 |

| Lingual braces | $8,000 – $10,000 | $333 – $417 |

With a $1,500 insurance benefit applied upfront, subtract $63 per month from any of these figures for a 24-month plan.

2. How Orthodontic Payment Plans Work

Most orthodontic offices structure payment in three parts:

- Records fee ($100–$350): Paid at the consultation or records appointment for X-rays, photos, and impressions. Usually non-refundable.

- Down payment (15–25% of total): Due at the bonding appointment when braces go on. Insurance benefits are typically applied here if the insurer pays upfront.

- Monthly installments: The remaining balance divided equally over the treatment period, billed on a set date each month.

The monthly installment period usually matches the expected treatment length. If your treatment runs 20 months, you get 20 monthly payments. If treatment finishes early (rare) or runs long (common), the office typically adjusts accordingly — treatment finishing early does not mean your payment plan ends early.

3. In-House Financing vs. Third-Party Lenders

In-house orthodontic financing is the default and usually the best deal. Most practices offer 0% interest on the balance during the treatment period. There is no application, no credit check, and no promotional period cliff.

CareCredit and LendingClub Health are third-party medical credit cards accepted at many orthodontic offices. They offer 0% APR for promotional periods of 6, 12, or 18 months. The catch: if the balance is not paid in full by the end of the promotional period, all accrued interest — at 26.99% from day one — is added to your balance retroactively. They are useful if you need a longer repayment window than the in-house plan allows, but understand the risk.

Personal loans through banks or credit unions offer fixed interest rates (typically 7–15% for good credit) with no deferred interest trap. They are a better option than CareCredit for balances you know you cannot pay off within the promotional period.

4. How Insurance Reduces Your Monthly Payment

If your dental plan covers orthodontics, the insurer pays a portion of the total fee — typically 50% up to a lifetime maximum. Most lifetime maximums run $1,000 to $2,000 per person.

The orthodontic office submits a claim at the start of treatment. Some insurers pay the full benefit immediately; others pay in installments alongside your treatment schedule. Either way, the benefit reduces your financed balance and therefore your monthly payment.

Example

- Total treatment fee: $5,200

- Insurance lifetime max: $1,500 (paid upfront)

- Your financed balance: $3,700

- 22-month plan: $168/month

Without insurance, the same treatment would run $236/month. The benefit saves $68/month — $1,496 total over the payment period.

5. Using FSA and HSA Funds for Monthly Payments

Braces qualify as a medical expense under IRS guidelines, which means FSA (Flexible Spending Account) and HSA (Health Savings Account) funds can be used to pay for any portion of treatment — the down payment, monthly installments, or the full balance.

The most tax-efficient approach: use FSA funds to pay the down payment or large installments (since FSA funds expire annually), and use HSA funds for ongoing monthly payments (since HSA funds roll over indefinitely).

A $5,000 braces bill paid entirely with pre-tax FSA or HSA dollars saves $750 to $1,500 in taxes depending on your marginal rate — the equivalent of getting 15 to 30% off the total cost.

6. How to Lower Your Monthly Payment

- Negotiate a cash-pay discount: Many orthodontists offer 5–10% off the total if you pay in full at the start of treatment. On a $5,000 bill, that is $250–$500 off — which also shrinks any remaining balance you need to finance.

- Extend the payment period: Some practices allow payments beyond the treatment end date, reducing monthly amounts at the cost of a slightly longer payment commitment.

- Coordinate dual insurance coverage: If both spouses have orthodontic coverage, coordinating both benefits can significantly reduce the financed balance before monthly payments begin.

- Start treatment before your deductible resets: If your plan year runs January to December and your deductible is already met, starting treatment in late fall means the insurer pays faster.