Does MetLife Cover Braces? Plan Payouts & PDP Plus Secrets (2026 Guide)

Quick Answer

MetLife PDP and PDP Plus dental plans typically cover 50% of orthodontic costs up to a lifetime maximum. PDP Plus offers a wider in-network provider selection. Benefits and maximums vary by employer contract. Request a Pre-Treatment Estimate (PTE) before beginning treatment to confirm your specific coverage and avoid unexpected out-of-pocket costs.

Part of our Braces Cost & Insurance Master Guide.

You sit in the dentist’s office, staring at a treatment sheet that reads $5,900. You hand the receptionist your denture with that signed clean blue mark, hoping it absorbs the bulk of this bill. You're probably asking: "Will MetLife pay for my braces?" or "How can I get my MetLife plan to cover Invisalign?"

The direct answer is: Yes, MetLife dental plan cowl braces—best under any precise situations. Because MetLife administers a stack of custom organization-supported applications, your precise payment is governed using a complex device of lifetime caps, community levels, and strict age constraints. If you don’t know how your unique policy handles dental claims, you could easily end up paying the entire bill yourself.

In this guide, we will unpack MetLife’s orthodontic benefits. We’ll show you how to read your policy, calculate your exact out-of-pocket costs, and exploit MetLife-specific rules to maximize your coverage.

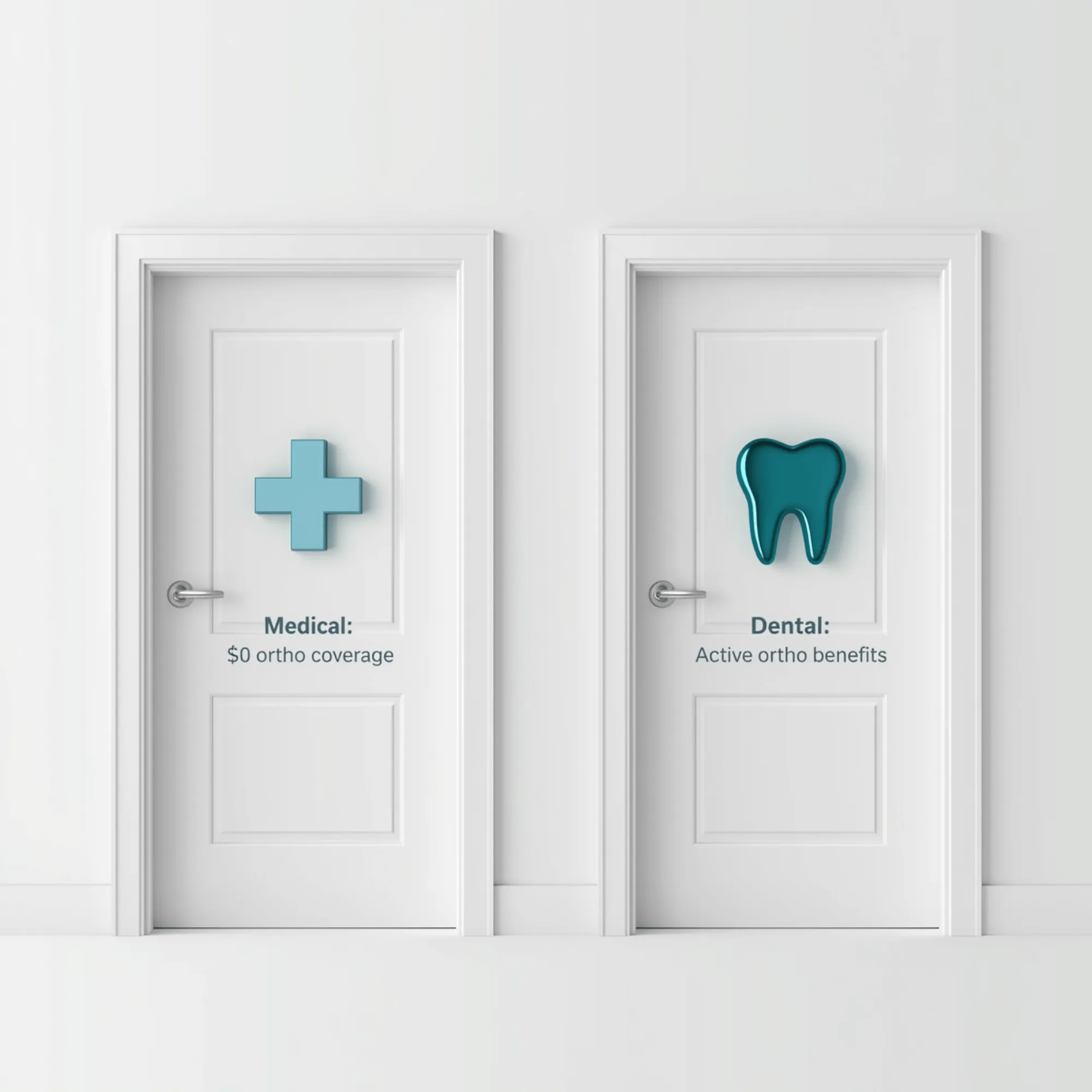

MetLife Medical vs. Dental: The Division Wall

A common mistake patients make is assuming their medical plan will step in to cover orthodontic care.

- Medical Insurance Limit: If you hold a MetLife Clinical Card, the dental insurance restriction is $zero. MetLife Medical will pay for best-in-class dental treatment if there is far part of complex jaw reconstructive surgery (orthognathic surgery) to correct extreme congenital malformations or trauma.

- The Dental Network Routing: All standard braces claims must run through your dental plan, managed by MetLife Dental. Your orthodontist must submit claims to MetLife Dental’s specific address using the correct ADA dental procedure codes (such as D8080 for kids or D8090 for adults), rather than medical billing channels.

PDP vs. PDP Plus: The Two Payout Systems

Your out-of-pocket cost is dictated by whether you have a MetLife PDP (Preferred Dentist Program) or a MetLife PDP Plus plan. The differences between these two options are massive.

1. MetLife PDP Plus

This is MetLife's most common plan type. It offers you the freedom to choose any certified dentist, but you have the most cash to stay in network.

- Percent Payment: MetLife PDP Plus plans typically cover 50% of dental expenses.

- PDP Plus Network Discount Advantage: In-network MetLife orthodontists agree to cap fees called the Negotiated Fee Schedule. If the out-of-network issuer costs $6,000, but the allowable charge within the MetLife community is $4,500, then 50% of your coverage will start from that reduction charge. You are shopping $1,500 well away from the community cut price before MetLife can also pay a dollar of the announcement.

2. MetLife PDP (Standard / HMO)

This is MetLife's managed care option. You are required to choose a primary dentist within the network, and you have to get a referral to see a participating dentist.

- Copayment Structure: Instead of paying percentages, MetLife's HMO uses hard and fast copay listing. You pay a fixed fee—usually $1,800 to $2,500—for a full live treatment.

- No Lifetime Limit: Unlike PDP Plus, HMOs do not have a whole life maximum cap. If your remedy lasts longer than forecast, you will not be charged extra. However, finding an orthodontist who accepts MetLife's HMO can be difficult, as the patient network is very restricted.

Pre-Treatment Estimate (PTE) Protocol

MetLife employs a rigorous review system known as the Pre-Treatment Estimate (PTE).

Although a few dental insurance corporations deal with prognosis as an elective, MetLife strongly recommends submitting a PTE for any treatment plan over $1,000.

Here is the exact step-by-step procedure for MetLife PTE:

- Diagnostic Submission: Before your bands or brackets are placed, your orthodontist sends your diagnostic X-rays, photos, plaster models, and treatment plan directly to MetLife.

- Clinical Review: MetLife's dental specialists compare the case to verify "orthodontic need" based on MetLife's clinical tips.

- Early Start Risk: If you begin energetic dentistry earlier than MetLife techniques and return a PTE, MetLife reserves the appropriate to audit the claim later. If they decide the case did not meet their scientific criteria, they can reject the claim entirely, leaving you responsible for the entire balance.

Calculation of your lifetime dental maximum (LOM)

MetLife PPO plans positioned strict Lifetime Orthodontic Maximum (LOM) into impact. This is a whole existence dollar restrict related to the member. Once MetLife will pay you this quantity closer to your dental care, that gain is completely exhausted for the relaxation of your lifestyles.

- Standard Cap Limit: Most business enterprise-sponsored MetLife plans function a whole lifestyles restriction of $1,000 to $2,000.

- Understanding the maths: If your braces rate $5,000, the 50% advantage charge shows that MetLife need to pay $2,500. However, in case your plan has a $1,500 lifetime restriction, MetLife will restriction their payout to $1,500. The closing $3,500 want to be paid.

Real-World MetLife PDP Plus Payout Breakdown:

| Fee Component | In-Network Orthodontist | Out-of-Network Orthodontist |

|---|---|---|

| Orthodontist's Standard Fee | $6,000 | $6,000 |

| MetLife Allowed Rate (Negotiated) | $4,500 | $6,000 (No Discount) |

| MetLife Payout Rate | 50% | 50% |

| Calculated Payout | $2,250 | $3,000 |

| Plan Lifetime Max Cap | $1,500 | $1,500 |

| MetLife's Actual Payout | $1,500 | $1,500 |

| Your Total Out-of-Pocket | $3,000 | $4,500 |

By selecting an in-network MetLife provider, you save an extra $1,500 out of pocket because the doctor is contractually obligated to write off the difference between their standard fee and MetLife's allowed rate.

MetLife's Rules on Invisalign & Clear Aligners

Yes, MetLife PDP Plus plans cover Invisalign on the same basis as standard metal braces. MetLife will apply your 50% coverage rate and lifetime maximum to clear aligner therapy.

However, you must watch out for these specific MetLife exclusions:

- No Direct-to-Consumer Aligners: MetLife policies exclude mail-order or DIY clear aligner kits. Your treatment must be fully managed in-person by an approved dentist or orthodontist.

- Non-Covered Align Upgrade Fees: Many dentists charge a premium "Invisalign lab fee" (between $500 and $1,500) over the cost of standard braces. MetLife treats this as a cosmetic upgrade. They will not pay for the lab fee; it is passed directly to you as a patient responsibility.

The Adult Orthodontic Rider and Waiting Periods

If you want braces for an adult (age 19 or older), you should review your policy information for Adult Orthodontic Rider.

Standard MetLife dental coverage plans limit orthodontic insurance based children to under nineteen years of age. If your corporation has not decided to shop for an individual rider, MetLife will deny any individual's braces claim at once.

Waiting time delay:

Many individual MetLife plans or small organization groups require a 12-month waiting period for major services, including dental care. You cannot commence a remedy or place a claim at any time during those first 12 months. If your child turns eighteen when signing up, they may be of age (reaching 19) before the readiness period ends, leading to a complete denial of benefits.

Stacking Insurance: MetLife Coordination of Benefits (COB)

If your circle of relatives has dual insurance (e.g., you have a blanket under a Cigna plan and your partner has Delta Dental), you can combine those blessings to reduce out-of-pocket fees.

However, MetLife has strict Coordination of Benefits (COB) rules:

- Primary vs. Secondary Rule: The primary plan is decided using the "birthday rule" (number one for kids determining whose birthday falls earlier in the year). The primary plan may pay first.

- Uniqueness Clause: Most MetLife plans include a "non-duplication of benefits" clause. If the primary plan (e.g., Delta Dental) pays 50% of the cost, MetLife (because it is the secondary plan) will assess its individual legal responsibility. Since MetLife's popular benefit is also 50%, they will determine that the primary plan has already met that restriction and can pay $zero.

- The Lifetime Max Cap Limit: Even outside of the non-duplication clause, duplicate plans will never pay more than most of their lifetime orthodontics.

Before committing to treatment, ask your orthodontist's billing department to submit a pre-determination request to both companies to get a clear estimate of your dual-coverage coordination.

Your Action Plan for MetLife Braces Coverage

Before scheduling your first adjustment, use this checklist to confirm your benefits:

- Check community calls on your card. Search for "PDP Plus", "PDP Select", or "MetLife DHMO".

- Call MetLife support directly. Ask: "Does my accurate planning include orthodontic benefits for adults (age 19+), or is it limited to youth?"

- Verify your final lifetime maximum. Ask: "What is the maximum balance of my remaining lifetime collection of teeth?"

- Ask for approximate waiting intervals. Ask: "Is there a waiting period for dental services, and when does it expire?"

- Verifying your issuer's community level. Confirm whether or not they are within the "PDP Plus" level (which offers the deepest discount).

- File a pre-treatment estimate (PTE). Make sure your orthodontic practice submits a full PTE package deal and gets written approval from MetLife before your braces are fitted.

Summary

Having MetLife insurance can significantly lower your orthodontic bills, saving you up to $1,500 on PDP Plus plans. To avoid unexpected bills, make sure you verify your age riders, submit a PTE, and stay inside the PDP Plus network.

Want to learn more about budgeting for your orthodontic care? Read our comprehensive Braces Cost & Insurance Master Guide or check out our guide on Using HSA or FSA funds for Braces to pay your remaining balance with tax-free dollars.